Major infrastructure projects strategy

The SERV major infrastructure projects Strategy (GIP Strategy): A groundbreaker for Swiss SMEs in the international market

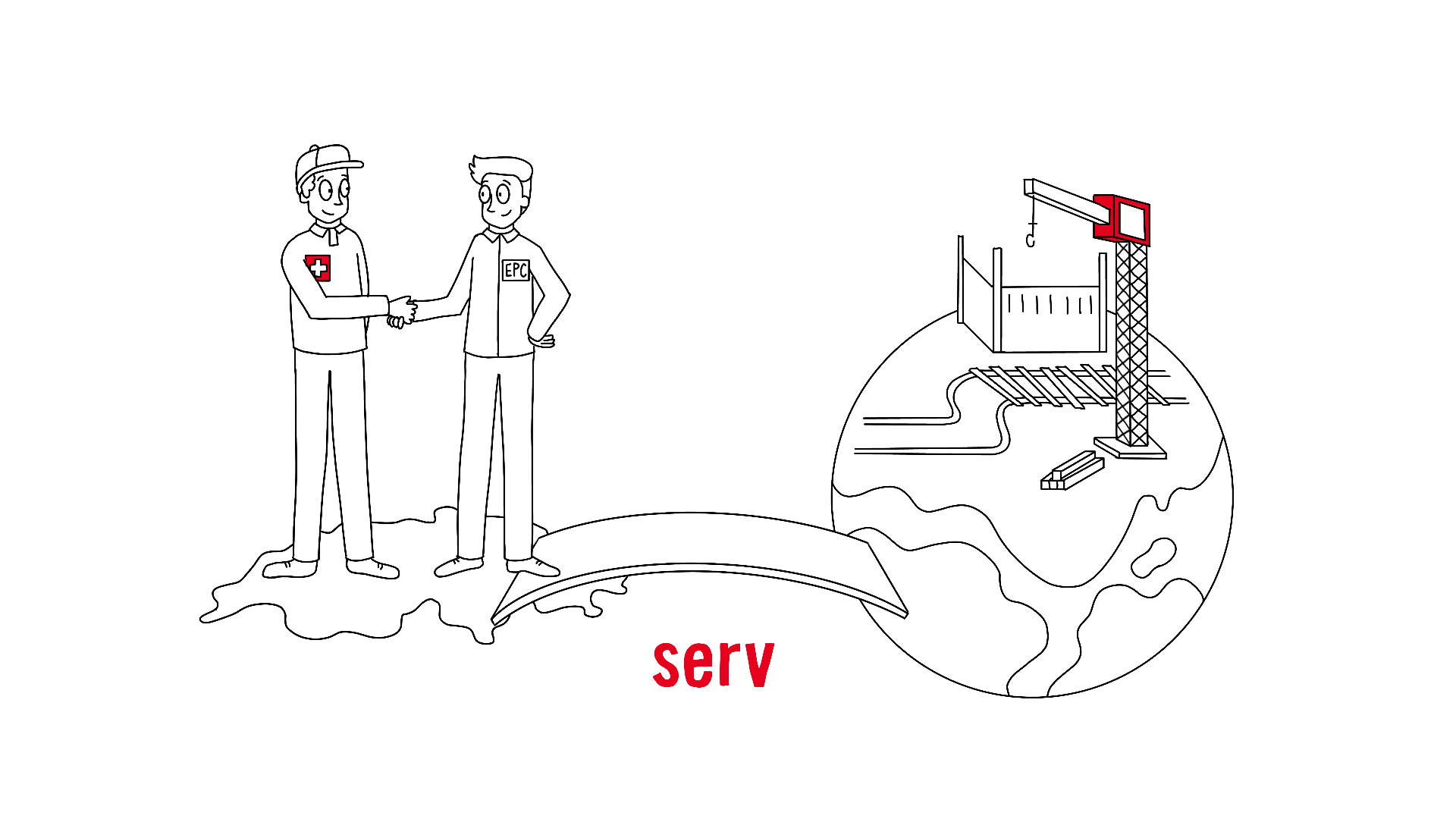

SERV helps Swiss SMEs achieve success in global markets. Through our major infrastructure projects (GIP) Strategy, we offer a unique service that facilitates access to major international projects for Swiss SMEs and strengthens their competitiveness.

Strategic partnerships for global projects

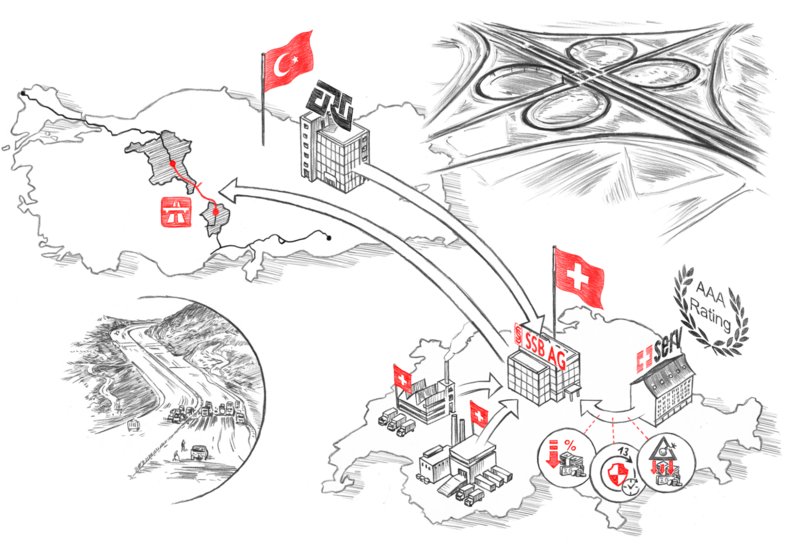

Demand for extensive infrastructure projects is growing worldwide. We support Swiss SMEs by using our global network to bring them together with international general contractors (EPCs). Our support enables SMEs to participate in major international projects, even if they lack their own extensive networks or resources to complete the acquisition. For example, our support was key to the participation in building a 330 kilometre-long motorway in Türkiye.

Client success stories

Comprehensive support and security

Our role does not just involve providing contacts. SERV performs thorough due diligence checks on projects and EPCs. We evaluate risks and ensure compliance with sustainability criteria and international standards. This creates a solid basis for Swiss SMEs to participate in large projects without having to bear the financial risk themselves.

Payment guarantee through SERV

Another key advantage of our support is payment security. SERV enables direct payments from the bank to Swiss exporters, thereby excluding the risk of non-payment by the EPC. As a result, SMEs don’t need to worry about financial uncertainty, and can focus on their core skills and completing the project instead.

Strengthening access to major international projects

The major infrastructure projects (GIP) mandate is an initiative by the Swiss Government and is co-financed by SECO. The aim is to facilitate access to major international infrastructure projects for Swiss exporters.

Team Switzerland Infrastructure was created with the specific aim of strengthening the competitiveness of the Swiss export industry in this challenging environment. The network brings together key players from industry and export promotion:

- Industry associations Swissmem, Swissrail and suisse.ing

- Export and location promotion organisation Switzerland Global Enterprise (S-GE)

- SERV

SERV’s GIP Strategy is an integral part of this mandate. It helps Swiss companies to sustainably strengthen their position in global infrastructure markets.

You can find further information about Team Switzerland Infrastructure here.

Better access to major international projects for Swiss SMEs

The video explains how SERV connects general contractors with Swiss SMEs and why the GIP Strategy creates a win-win situation for everyone involved.

Questions? Contact: